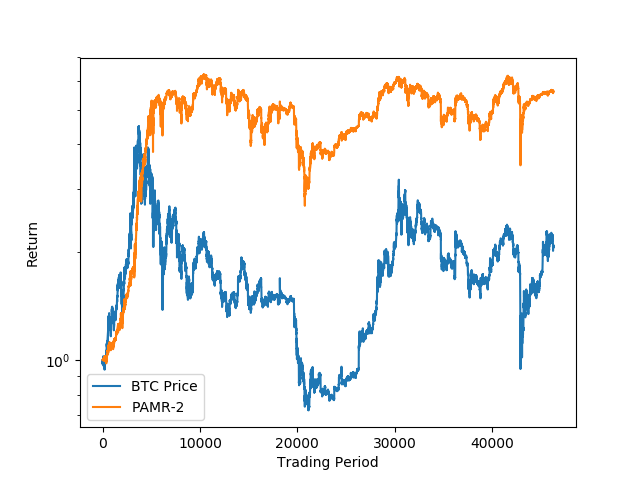

Implementation of PAMR and MAMR portfolio management algorithms for analysis and online portfolio management of cryptocurrency assets.

Parameters fitted to maximise the mean daily return, algorithm runs every 30 minutes

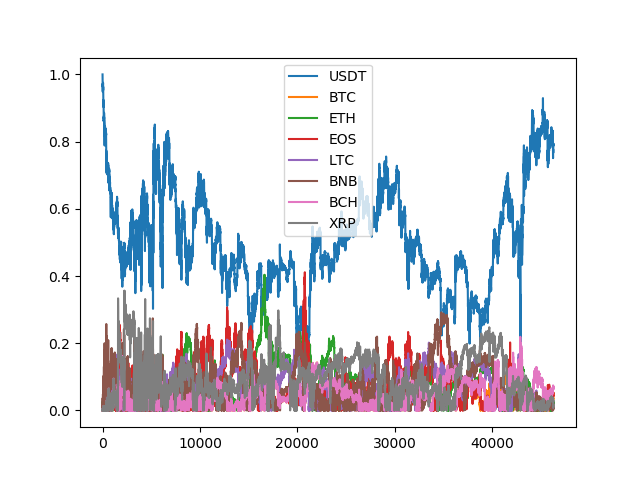

Current portfolio consists of 8 large market cap coins.

pip3 install requests numpy scipy

git clone https://github.com/alfredholmes/binancePAMR.git

cd binancePAMR

python3 data/get_candles.py

python3 analysis/PAMR.py

Li, B., Zhao, P., Hoi, S.C.H. et al. PAMR: Passive aggressive mean reversion strategy for portfolio selection. Mach Learn 87, 221–258 (2012). https://doi.org/10.1007/s10994-012-5281-z https://link.springer.com/content/pdf/10.1007/s10994-012-5281-z.pdf

Peng, Zijin & Xu, Weijun & Li, Hongyi. (2020). A Novel Online Portfolio Selection Strategy with Multiperiodical Asymmetric Mean Reversion. Discrete Dynamics in Nature and Society. 2020. 1-13. 10.1155/2020/5956146. http://downloads.hindawi.com/journals/ddns/2020/5956146.pdf